Swing Trade Ideas – October 31, 2025

Laurie’s Abbreviation Index:

** ‘div’ – dividend

** ‘m/m’ – month over month

** ‘y/y’ – year over year

** ‘Inven’ – inventories

** ‘mfg’ – manufacturing

** +/- – plus or minus, positive or negative

** Underlined text – higher volume premarket

** ‘d’ – day

** ‘Y’ – year

**govt – government

Color Key: Positive – Neutral – Negative

Global Markets: USA, Europe, Japan, China, Hong Kong – Slight negative set-up

· Commodities: Gold, Silver, Oil, natgas, AGGS, Industrial Metals, Bitcoin

· Yields: 30Y Bond -0.29% Currencies: USA$ -0.01%, CAD -0.16%, YEN-0.71%, BTC/USD-0.5% Vix:18.6

· Stocks: GOOGL+8.4%,

NOW+2.9%, LLY+3.2%, GH+23%, AAP+19.6%, INSM+10%, MSFT-2%, META-9%, CMG-16%,

MRK-2.8%, SBUX-3.3%, BAX-10%, CVNA-8%, RBLX-5% EPS

Events:EUR: Rate decision, expect no change

Equity: Global indices ex-japan are lower post FOMC, MAGS earnings and

China tariff meeting. FOMC is divided on need for rate cuts and Powell reduced

Dec rate cut expectations. FED will stop QT in Dec and there is chatter that

FED will need to add liquidity as some cracks are forming. China-USA trade

talks were generally a can kicking exercise with China buying soybeans again, a

reduction in USA tariffs by 10% and a 1y delay in critical metals export

restrictions. The critical metal spec companies are higher in reaction. MAGS

earnings reactions are mixed with GOOGL moving higher than the expected move,

META moving lower than the expected move and MSFT moving lower. Issue with META

is an increase in spending and outpacing revenue. MSFT beat expectations but

discussed higher capex. GOOGL revenue growth is deemed to be outperforming

capex. In theory the insatiable datacenter building is positive for semis

however NVDA AMD are lower potentially since the QQQ is lower or it’s not clear

(to me) that there is any change to the status quo on China visa vis export

controls. CMG and SBUX lower so maybe consumers not buying enough overpriced

food but QSR higher so Tim Hortons working:) Some healthcare names LLY, CAH, GH

higher lifting the XLV. NVO buying MSTR lifting MSTR. NOW higher with good

earnings and a 5:1 stock split, may be worth a look. The macro reaction to the

FOMC is yields higher and US$ higher. The move in the US$ is negative for

foreign equities and notable is KWEB -1.9% post the XI-Trump meeting. SPX

6900 is the bull/bear level and SPX is currently below. Positioning in indices

and many single stocks has been heavily tilted to calls and should stocks fail

to rise, the expiration of out of the money calls will be a negative weight.

Also, the heavy retail speculation in leveraged ETFs will increase volatility

in both directions.

SPY 685.4 Resistance 687 690 692 Support 685 683, QQQ 633.9 Resistance

637 640 Support 631 630 627

Daily Expected Move. SPX(6932-6849), SPY(692-683), QQQ(644-627),

IWM(250-243)

Stocks to watch GOOGL, NOW, META, MSFT, CMG, SBUX Speculative CVNA, MTSR, CRML

Indices SLV, GDX, GLD, XBI, XLV, ARKG, UNG, US$, KWEB, IBIT,

XLY, /CL, TLT, ETHE, MAGS

S&P500 GOOGL, FMC, CMG, META, MSFT, FI

Other MTSR, CRML, USAR, MP, CLF, STLA, OKLO, NVO, JD, BABAGlobal Markets: USA, Europe, Japan, China, Hong Kong – Slight positive set-up

· Commodities: Gold, Silver, Oil, natgas, AGGS, Industrial Metals, Bitcoin

· Yields: 30Y Bond -0.19% Currencies: USA$ +0.14% CAD -0.26% YEN-0.07% BTC/USD+3.7% Vix:18.45

· Stocks: AAPL+1.8%,

AMZN+12.7%, RDDT+9%, XOM-1.5%, CMCSA-1.9%, DXCM-10%, LUMN-5%, ROKU-3.5%, EPS NFLX+2.4% stock

split

Events:EUR: CPI > expectations China: mfg PMI weakening

CDN: GDP USA: Chicago PMI and FOMC speakers

Equity: USA large cap indices higher driven by AMZN and AAPL earnings

with AMZN move in 3x the expected move and AAPL moving to the expected move.

AMZN AWS strength and plans for continued Capex is the greenlight for algos to

bid up the AI/semi basket. Usual semi-suspects NVDA, AMD, MU and AI names PLTR

ORCL have the Pavlovian buy. MRVL is higher since they will make chips for

AMZN, worth watching. China mfg data was weak which is weighing on the China

indices. RDDT large move higher on AI revenue, worth watching. Bitcoin is

having the usual end-of-month move higher, lifting the basket of miners and

treasury companies. SPY and QQQ are above the daily expected move, hence

potential to squeeze higher or stall out. Typically when there are large moves

by a few large caps, the remainder of the market is subdued or lower.

Volatility may fall as is common on a Friday, especially since the MAGS

earnings, the China tariff discussion and the FOMC meeting are done. Generally,

this is positive for equity with the short-term issue the govt shutdown.

Main thing to watch today is whether the MAGS/AI hold the post-earnings bounces

and whether indices remain above the upper expected move highs.

SPY 685.6 Resistance 688 690 Support 683 682 680, QQQ 634.8 Resistance

636 640 Support 632.7 630 625

Daily Expected Move. SPX(6861-6782), SPY(684-676), QQQ(632-620),

IWM(247-242)

Stocks to watch GOOGL, NOW, META, MSFT, CMG, SBUX Speculative CVNA, MTSR, CRML

Indices ETHE, IBIT, MAGS, UNG, XLY, ARKK, QQQ, XLK, QTUM, KWEB, GDX,

XLV, /CL, GLD, XLF, XLE

S&P500 AMZN, COIN, WBD, PLTR, NVDA, AMD, AAPL, ORCL, SMCI, MU, META, DXCM, XOM

Other RDDT, MSTR, BMNR, MRVL, IREN, NVTS, SBET, CRML, CIFR, NVTS, RIOT, MARA, LUMN, NVO, BABA, LI, JD

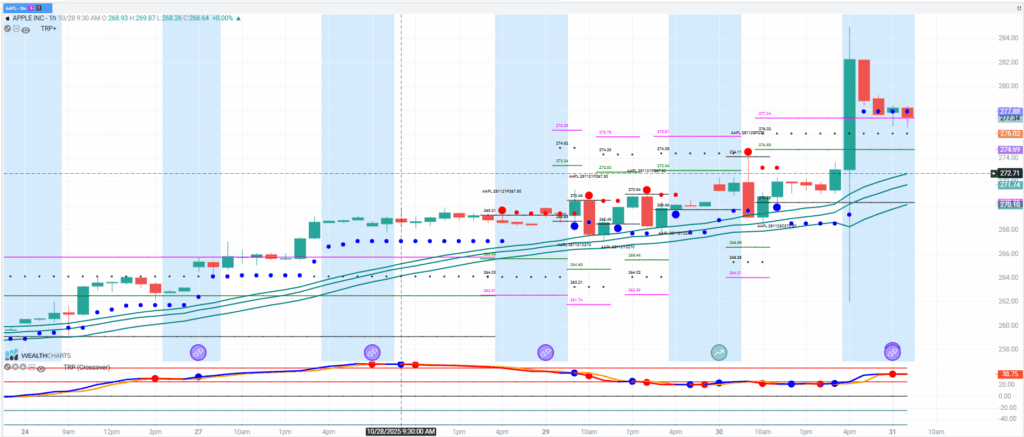

AAPL

AAPL higher on earnings that were IMO not impressive however stock is higher on rosy outlook for iPhone17 refresh cycle. Straddle approach today with 275.5 the bull/bear level with 280 target above and 275, 270 targets below.