Swing Trade Ideas – March 6, 2026

Laurie’s Abbreviation Index:

** ‘div’ – dividend

** ‘m/m’ – month over month

** ‘y/y’ – year over year

** ‘Inven’ – inventories

** ‘mfg’ – manufacturing ** +/- – plus or minus, positive or negative

** Underlined text – higher volume premarket

** ‘d’ – day

** ‘Y’ – year

**govt – government

Color Key: Positive – Neutral – Negative

Global Markets: USA, Europe, Japan, China, Hong Kong – negative set-up

· Commodities: Gold, Silver, Copper, Palladium, Oil, natgas, AGGS, Bitcoin

· Yields: 30Y Bond -0.48% Currencies: USA$ +0.16%, CAD +0.02%, YEN -0.28%, BTC/USD-0.67%, Vix:21.45

· Events:USA:

NFP payrolls, retail sales 830ET

Stock News: PBR+3.17%, MRVL+12%, IOT+10%, SWBI+12%, COST-0.4%,

GAP-8%, MEOH-7.5% Earnings

· Equity: Global indices are lower premarket ahead of USA NFP and retail sales. European GDP lower than expected adds to energy cost fears. SPX positioning remains in negative gamma with 6800 a pivot level and potential for lows into 6600s and a high of 6900. Usually, NFP is a market-moving event with the IV falling post-report and a bounce on an inline+ report, but now the concern is Iran war and the propensity of Trump for weekend shenanigans so a NFP bounce, should it come, may be transitory. MAGS are weak with NVDA leading to the downside, and SMH is generally weak and underperforming IGV software. There has been an unwind of the long semi-short software trade, but need to watch whether the trade continues. My conspiracy theory is that the damage to the Gulf states will impact both announced AI investments in the USA and the Gulf, which can impact the AI hardware names. Oil continues higher, and IMO is not pricing in the worst case but is raising inflation concerns, which is negative for bonds and yield-sensitive equities like staples. US$ has been rising and causing an unwind of the US$ debasement trade i.e. foreign equities. Many countries are energy importers, and the rising energy prices with no end in sight is damaging for Europe, Korea, Japan and some emerging markets. Credit spreads are rising, and private credit continues to be a risk and may be spilling into financials. But despite the negatives, the USA equity market has so far held up with 0DTE put sellers who have stepped up daily to support markets and call sellers who dampen the upside. Today, look for the same behaviour with the caveat that one day the put sellers may not step up, probably if there is a vol spike. Post earnings names to watch: MRVL, IOT, COST, GAP. MAGS in play as usual with NVDA close to the key 180 level and worth watching with semi weakness. ** US NFP -92k UE rate 4.4% vs 4.3%. Reaction: equity lower, TLT higher, US$ lower

·

Stock MRVL, OXY, CF, NVDA, AMZN, AMD Speculative IOT, GFI

Indices /CL, UNG, KWEB, XLE, MSOS, SLV, GLD, UUP, GDX, ETHE,

IBIT, SMH, FEZ, ARKK, XLK, EFA, QQQ, IWM, MAGS

S&P500 DOW, OXY,

CF, APA, DVN, EQT, COP, FANG, MOS, EOG, COO, GLW, CCL, AMAT, UAL, LRCX, RCL,

MRNA, KLAC

Other MRVL, IOT, JD, VG, PBR, PDD, EQNR, XPEV, STM, GFI,

PONY, CIFR, DHT, AG, SBSW, APLD, QBTS, COHR, LITE

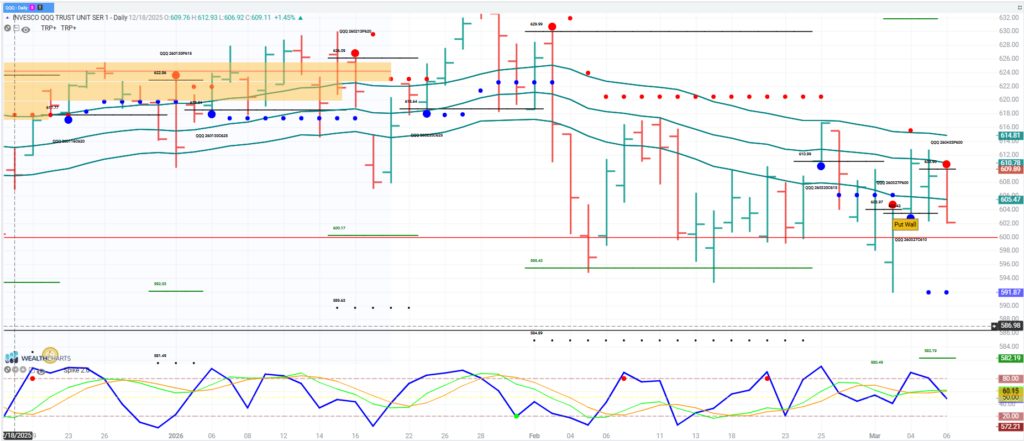

QQQ

QQQ is pulling back post the weaker NFP jobs report and high UE rate data, but has been declining since the European open. Currently 602, the bottom of the daily expected move is 601.5 and put wall is 600. The put wall is a good reference level for bounce or breakdown with the next major option level below 595 and upside 605, 607 targets and upper daily expected move 616. Potential for bounce off the open as shorts monetize and then the question is whether the bounce continues or shorts re-enter. Semis were weak premarket and worth watching today for a bounce or further selling.